The article is written by Adv. Siddhant Jain.

Key Points

A term sheet is a non-binding document that outlines the key terms of a startup investment before formal agreements are drafted. This comprehensive guide covers:

- What a term sheet is and its legal nature in India

- 16 critical clauses every term sheet must address — from valuation and share structure to anti-dilution, exit rights, and dispute resolution

- Key considerations for founders, investors, and legal counsel

- Real-world examples and a landmark Delhi High Court ruling (Zostel v Oravel)

Whether you are a startup founder, investor, or legal professional, this guide will make you term sheet-ready.

Introduction: Why Term Sheets Matter in the Startup World

In the startup ecosystem, where bold ideas meet ambitious capital, the term sheet is your foundational map. Whether you are a lawyer stepping into startup practice, an early-stage founder gearing up for a funding round, or a seasoned investor hunting the next unicorn — understanding term sheets is not optional. It is your competitive edge.

Picture this: your groundbreaking idea has finally caught the attention of a high-profile investor. Excitement fills the air. But before the celebrations begin, there is one critical document to navigate — the term sheet. Think of it as the architectural blueprint of your investment deal: it outlines the fundamental terms and conditions that will shape your company’s future without drowning you in legal complexity.

This article demystifies term sheets from a commercial perspective, keeping legal jargon to a minimum while ensuring you walk away with actionable insights. We will cover what a term sheet is, its legal nature, the key clauses it must contain, and what each stakeholder — founders, investors, and legal counsel — should prioritise.

Note: This article assumes some familiarity with startup terminology. For any unfamiliar terms, refer to the footnotes provided at the end.

What Is a Term Sheet? A Clear Definition

A term sheet is a non-binding agreement that sets out the basic terms and conditions of a proposed investment. It acts as a precursor to formal, legally binding documents and serves as the negotiation framework that guides lawyers when drafting definitive agreements to finalize a transaction.

Purpose of a Term Sheet

A well-drafted term sheet accomplishes four key objectives:

- Clarify Intentions: Establishes mutual understanding of investment terms between all parties.

- Facilitate Negotiations: Provides a structured framework to discuss, refine, and finalise deal terms.

- Save Time and Legal Costs: Identifies potential deal-breakers early, avoiding expensive disputes later.

- Provide a Transaction Roadmap: Guides the preparation of final binding agreements such as Share Purchase Agreements (SPA) and Shareholders’ Agreements (SHA).

Parties Involved in a Term Sheet

Three primary stakeholders are involved in every term sheet:

- The Investor: The entity or individual providing capital.

- The Target Company: The startup or business receiving the investment.

- Legal Counsels: Lawyers representing both the investor and the target company to ensure legal precision.

The Legal Nature of Term Sheets in India

No specific law in India defines the legal nature of a term sheet. Its binding effect depends entirely on its content and the intent of the parties involved. Understanding this nuance is critical.

Non-Binding Term Sheets

Non-binding term sheets are the most prevalent in the Indian startup ecosystem. They serve as a negotiation framework — setting out proposed terms without creating formal legal obligations. However, non-binding does not mean consequence-free.

Key characteristics:

- Flexibility to explore deal feasibility without legal commitment.

- Certain clauses within a non-binding term sheet can still be legally binding — most commonly confidentiality, exclusivity, no-shop clauses, and dispute resolution provisions.

- Non-compliance with binding sub-clauses can attract legal consequences.

Binding Term Sheets

Though less common, binding term sheets create a formal legal commitment between parties. Breaching such a term sheet can lead to litigation. These typically precede definitive agreements like SPAs or SHAs.

Landmark Judgment: Zostel Hospitality v. Oravel Stays (2022)

The Delhi High Court, in Zostel Hospitality (P) Ltd. v. Oravel Stays (P) Ltd. [2022 SCC OnLine Del 455], held that even where a term sheet expressly states it is non-binding, if its clauses create specific obligations and the parties take steps to fulfil those obligations, the term sheet can be construed as legally binding. This judgment underscores the importance of precise drafting — labels alone do not determine enforceability.

Bottom line: Whether a term sheet is binding or not ultimately depends on (i) what it says and (ii) what the parties intended when they signed it.

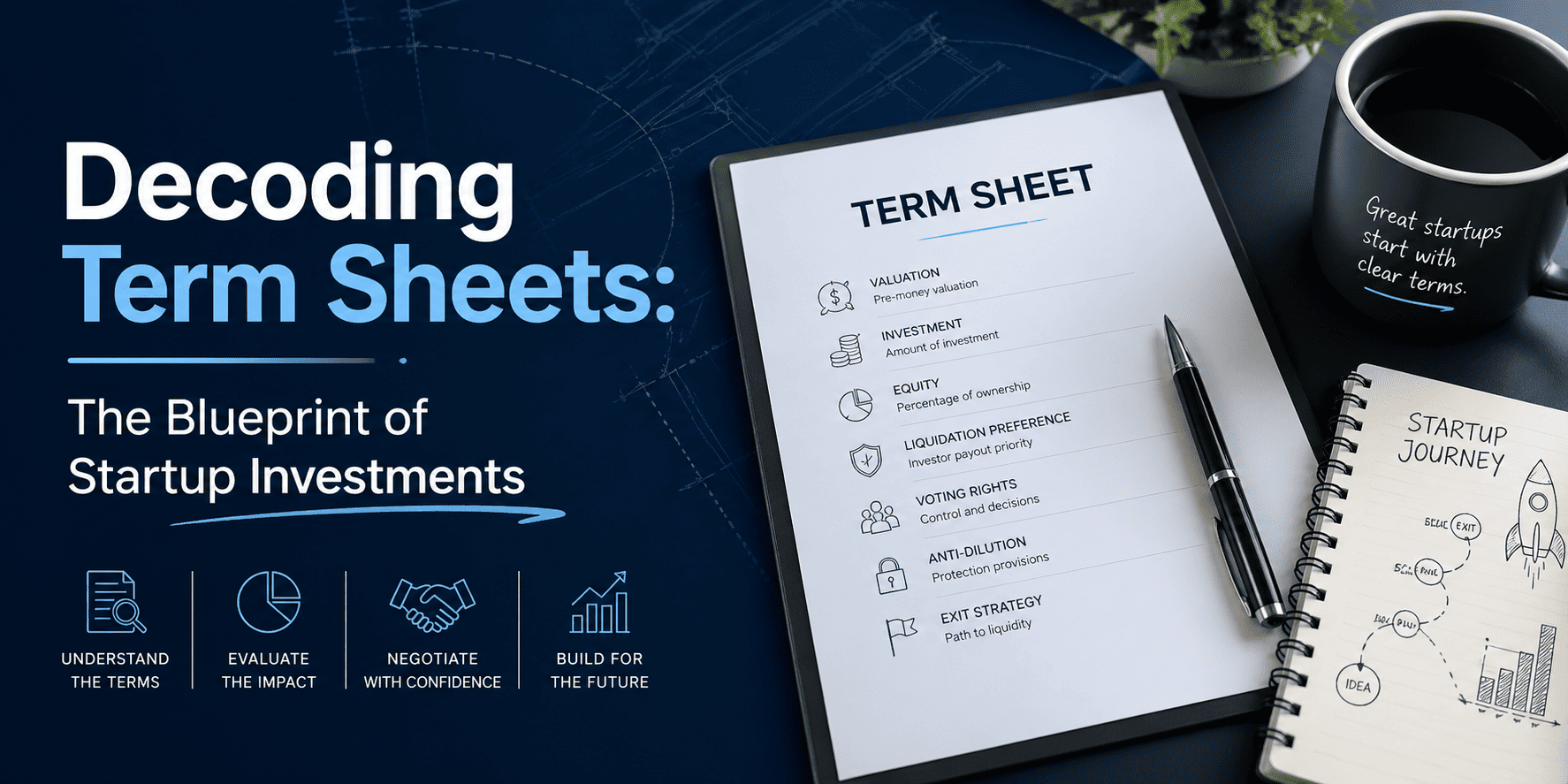

Drafting a Term Sheet: 16 Key Clauses Explained

To illustrate the practical drafting of a term sheet, consider a scenario where a startup is issuing equity shares to an investor in a funding round. Here are the essential clauses to include:

1. Nature of the Term Sheet

This section explicitly states whether the term sheet is binding or non-binding. As a general rule, most term sheets are non-binding — except for specific protective clauses such as confidentiality and exclusivity.

2. Parties Involved

Clearly identifies the investor and the target company by their full legal names, contact details, and registered addresses. Clarity here prevents disputes about who is party to the agreement.

3. Company Valuation: Pre-Money vs Post-Money

Determining the company’s valuation is one of the most commercially significant decisions in the term sheet. The key choice is between:

- Pre-Money Valuation: The company’s value before the new investment. Commonly used for early-stage rounds (Seed, Series A). Helps determine the investor’s ownership percentage post-investment.

- Post-Money Valuation: The company’s value after the investment is made. More common in later-stage rounds (Series B and beyond). Offers investors clearer visibility of their stake’s relative value.

The right choice depends on the company’s stage, the investment round, and the negotiating dynamics between founders and investors. Neither approach is universally superior — context is everything.

4. Nature and Number of Shares Issued to the Investor

This clause defines the type of securities being issued and the resulting shareholding structure. It typically addresses:

Nature of Securities:

Investors usually receive preference shares, which carry special rights such as liquidation preference and anti-dilution protection. These rights are negotiated and specified in the term sheet.

Shareholding Patterns:

- Undiluted Stake: The shareholder’s percentage before conversion of convertible instruments (like ESOPs).

- Fully Diluted Basis: The shareholder’s percentage after all convertible instruments are converted into equity.

Example: Mr. A and Mr. B each hold 50% in XYZ Ltd. The company has issued ESOPs representing 10% of the share capital. On a fully diluted basis, A and B each hold 45%, with ESOP holders collectively holding 10%. If investor Mr. M acquires 25% on a fully diluted basis, the term sheet ensures Mr. M’s stake is not diluted even upon ESOP exercise — meaning A and B each drop to 32.5% on full dilution.

5. Investment Amount and Payment Terms

The term sheet must clearly specify the total investment amount and the mode of payment — whether it will be made as a lump sum or in tranches. If structured in tranches, each tranche must be explicitly defined along with the trigger event that releases it. Transparency here protects all stakeholders and avoids future disagreements.

6. Appointment of Director(s) to the Board

An investor’s right to appoint a director is generally proportional to their investment quantum. Depending on the investment size, the investor may receive the right to appoint an executive or non-executive director. Additionally, the term sheet may provide for an observer role — a nominee who can attend board meetings and receive notices but holds no voting rights.

7. Promoters’ Lock-In

When an investor commits capital, they are also betting on the founding team. The promoters’ lock-in clause ensures founders remain committed to the company for a specified period and cannot exit or dilute their stake without restriction. Key negotiation points include:

- Lock-in period: The duration during which founders cannot exit.

- Nature of lock-in: Whether it is a full lock-in (no dilution permitted) or a partial lock-in (allowing limited dilution in defined liquidity scenarios).

8. Fall-Away Rights

This clause is a direct corollary of the lock-in. Founders lock in their commitment on the basis that the investor also maintains a certain level of commitment (a defined minimum shareholding). If the investor’s stake falls below the agreed threshold — whether through sale or dilution in subsequent rounds — the founders’ lock-in obligations are released. This is one of the most heavily negotiated clauses in any term sheet.

9. Transfer Restrictions

Transfer restrictions govern the circumstances under which shareholders can transfer their securities to third parties. These clauses typically favour investor interests and take two primary forms:

- Right of First Offer (ROFO): The holder of this right must be offered the opportunity to purchase shares before they are offered to any third party. If the ROFO holder makes an offer, the selling shareholder may still sell to a third party — but not at a lower price than the ROFO offer.

- Right of First Refusal (ROFR): This gives the holder the right to match any third-party offer before the shares can be sold to that party. If the ROFR holder matches the offer, the seller is obligated to sell to them instead.

10. Anti-Dilution Provision

The anti-dilution clause protects investors when a startup raises additional capital at a lower valuation than a previous round (known as a down round). Without this protection, the investor’s ownership percentage shrinks, reducing the value of their investment.

There are two main types of anti-dilution mechanisms:

- Full Ratchet Anti-Dilution: The investor’s original share price is adjusted entirely to the new lower price. For example, if you purchased shares at ₹100 and the company issues new shares at ₹50, your shares are repriced to ₹50 — giving you more shares to maintain your ownership percentage. This is the most protective provision for investors but can significantly disadvantage founders and new investors.

- Weighted Average Anti-Dilution: A more balanced approach that adjusts the investor’s share price based on a weighted average of the new and old share prices, factoring in the number of new shares issued. This is the most commonly agreed mechanism as it balances protection for investors with fairness to founders and future investors.

From a commercial standpoint, anti-dilution provisions reassure investors while signalling to them that the startup is committed to protecting their interests. However, overly aggressive anti-dilution terms can deter future investors — so striking the right balance is essential.

11. Anti-Competition and Non-Solicitation Clauses

Investors place significant value on the founding team. They want assurance that promoters are fully committed to growing the target company and not simultaneously building competing ventures. This clause typically includes three components:

- Employment Terms: Specifies the founders’ primary obligations and time commitment to the startup.

- Anti-Competition Clause: Prohibits founders from directly or indirectly engaging in businesses that compete with the target company during a defined period and within a specified geography.

- Non-Solicitation Clause: Prevents founders from poaching the startup’s employees, clients, or business partners if they leave or launch competing ventures.

Clearly articulating these clauses at the term sheet stage reduces the risk of costly disputes during later drafting and prevents founders from diverting intellectual capital to competing ventures.

12. Affirmative Voting Rights / Reserved Matter Rights

Often described as the most important investor-protection clause, affirmative voting rights (or reserved matter rights) give investors veto power over specific high-impact decisions. No reserved matter can proceed without the investor’s prior written approval.

Common reserved matters include:

- Issuance of new shares or securities (which could dilute the investor’s stake)

- Taking on debt above a specified threshold

- Mergers, acquisitions, or sale of material assets

- Fundamental changes to the business model

- Capital expenditures beyond a defined limit

- Hiring or termination of key senior personnel

- Amendments to the company’s constitutional documents

While this clause is essential for investor protection, it must be crafted carefully to avoid creating operational bottlenecks. Setting clear thresholds — for example, defining what constitutes a ‘major expenditure’ — ensures that routine business decisions are not unnecessarily hampered.

13. Exit Rights

Every investor needs a clear path to realise returns on their investment. A well-structured term sheet defines multiple exit mechanisms:

- Initial Public Offering (IPO): When the company lists its shares on a recognised stock exchange, all shareholders — including investors — gain the right to sell shares publicly. Note that statutory lock-in requirements may apply post-listing.

- Trade Sale: The investor’s right to sell may be triggered when the company sells a stake to a strategic buyer, typically in the same industry.

- Tag-Along Rights: This provision protects minority shareholders by allowing them to join a selling majority shareholder’s transaction at the same price and terms — preventing them from being left behind when control changes hands.

- Drag-Along Rights: This right — typically held by majority shareholders or investors — compels all other shareholders to sell their shares if a prospective buyer offers to acquire the entire company at an agreed valuation. It streamlines exits and maximises returns.

- Share Buyback: The company may repurchase its own shares from shareholders as a financial consolidation measure. However, buybacks must be offered to all shareholders on a pro-rata basis due to statutory restrictions — the company cannot selectively buy back shares.

14. Liquidation Preference

In the event of a liquidation, sale, or winding-up of the company, this clause determines the priority order in which proceeds are distributed. Since most investors receive preference shares, they are entitled to their returns before common shareholders. Three types of liquidation preferences are typically negotiated:

- Straight Preferred (Non-Participating): The investor receives a fixed multiple of their original investment (e.g., 1x or 2x) before any proceeds are distributed to common shareholders. After receiving their multiple, they do not participate further in the remaining proceeds.

- Participating Preferred (Double-Dip): The investor first receives their investment multiple, and then also participates pro-rata in the remaining proceeds alongside common shareholders. This is the most investor-favourable structure. Example: An investor with a ₹20 lakh investment holding 10% and a 2x preference in a ₹2 crore exit first receives ₹40 lakhs, then 10% of the remaining ₹1.6 crore — a further ₹16 lakhs.

- Partially Participating Preferred: Similar to participating preferred, but the investor’s aggregate returns are capped at a defined amount. Beyond the cap, remaining proceeds go exclusively to common shareholders. This serves as a fair compromise between investors and founders.

15. Exclusivity Rights

The exclusivity clause grants the investor an exclusive window to conduct due diligence and finalise investment terms without the risk of competing bids from other investors. During this period, the target company is prohibited from negotiating with any other potential investor. This clause is typically binding and should specify: (i) the duration of the exclusivity period, (ii) any permitted exceptions or carve-outs, and (iii) the consequences of a breach.

16. Dispute Resolution

Disputes are an inherent risk in any commercial transaction. The dispute resolution clause determines how conflicts will be handled and is almost always binding in nature. Key decisions include:

- Method: Arbitration is strongly preferred in the startup world due to its confidentiality, speed, and efficiency compared to conventional litigation.

- Seat of Arbitration: This determines the legal jurisdiction governing the arbitration. Foreign investors typically push for internationally recognised seats such as Singapore, London, or New York. Indian startups generally prefer domestic seats such as Mumbai or Delhi. Neutral venues like Hong Kong or Dubai often serve as a compromise.

- Governing Rules: The arbitration rules to be followed, such as those of the International Chamber of Commerce (ICC) or UNCITRAL.

- Language of Proceedings: The language in which proceedings will be conducted.

A well-crafted dispute resolution clause keeps the startup venture on course even when disagreements arise, providing a clear, agreed-upon pathway to resolution.

Key Considerations for Each Stakeholder

For Startup Founders

- Clarity on All Terms: Ensure every term is precisely defined. Ambiguous language leads to misunderstandings that can derail funding rounds and damage relationships. Avoid unnecessary legal jargon — a good term sheet is clear, concise, and commercially grounded.

- Understand Future Implications: Anti-dilution provisions and liquidation preferences can significantly affect future funding rounds and the founders’ equity positions. Understand the downstream consequences of every clause before agreeing to them.

- Protect Governance Rights: Be strategic about board composition and reserved matters. Granting too many veto rights can paralyse decision-making; too few can leave investors feeling exposed. Balance is key.

For Investors

- Robust Anti-Dilution Protection: Ensure anti-dilution provisions are strong enough to maintain your ownership in future down rounds. Weighted average protection is the industry standard for balancing fairness with security.

- Clear Exit Strategy: Specify exit mechanisms explicitly. Include drag-along rights to ensure a streamlined exit if a majority sale opportunity arises.

- Adequate Governance: Secure board representation and meaningful reserved matter rights to safeguard your investment and maintain visibility into key decisions.

For Legal Counsel

- Precision in Drafting: Every clause must be unambiguous. Define key terms explicitly. Use non-binding language for substantive commercial terms while ensuring protective clauses (exclusivity, confidentiality, dispute resolution) are binding.

- Strategic Negotiation: Help clients understand the commercial implications of each clause and negotiate terms that protect their interests without making the deal unattractive to the other party.

- Regulatory Compliance: Ensure the term sheet complies with applicable corporate law, securities regulations, FEMA (if foreign investment is involved), tax laws, and any industry-specific requirements. Include contingencies to address issues that may arise during due diligence.

Conclusion

Navigating the startup investment landscape without a firm grasp of term sheets is like setting sail without a map. Term sheets are more than administrative formalities — they are the commercial and legal blueprint of your entire investment journey. They set the negotiating stage, establish mutual expectations, and lay the groundwork for legally binding agreements that can define a company’s trajectory for years.

For founders, it means gaining clarity on terms and understanding how provisions like anti-dilution and liquidation preferences will influence future fundraising. For investors, it means securing robust protections through carefully crafted exit rights, governance mechanisms, and anti-dilution provisions. For legal counsel, it means drafting with precision, negotiating with strategy, and ensuring every clause serves the client’s best interests.

The devil is always in the details. A meticulously crafted term sheet paves the way for a thriving, mutually beneficial partnership — one where ambitions align, interests are protected, and the path to success is clearly charted.

Need Legal Assistance?

If you require assistance with term sheet drafting, startup investment documentation, or any other legal services mentioned in this article, feel free to email us at contact@vakalattoday.com. If you have any legal queries or require legal assistance, you can book a consultation directly: Click Here to schedule a 30-minute session.

Disclaimer: This article is intended to provide a general guide to the subject matter and does not constitute legal advice. Specialist legal advice should be sought for your specific circumstances.

Exciting Update!

Vakalat Today has launched its official WhatsApp Channel to share quick legal insights, compliance tips, and updates on startup-related laws — all in one place.

Join the channel here: https://whatsapp.com/channel/0029Vape2tC5K3zczcnYzb2x

Meet Siddhant Jain — a lawyer who thrives in the dynamic world of Business & Commercial Law, Private Client Practice, and Maritime Matters. For him, boardrooms are battlefields, mergers are puzzles, and corporate jargon is a second language. Whether it’s navigating the maze of company law, tackling securities regulations, steering businesses through the stormy seas of bankruptcy and insolvency, or handling complex maritime disputes, Siddhant has done it all.

Beyond the corporate hustle, Siddhant also works closely with private clients — advising on wills, Trust, family settlements, agreements, and bespoke legal strategies to safeguard both business and personal interests.

From drafting intricate legal opinions on mergers to guiding company closures, and from advising shipping stakeholders to assisting families in succession planning, his practice spans a diverse legal spectrum. And when he’s not solving legal riddles, Siddhant shares his insights through newsletters and publications — because why should only his clients benefit from all that knowledge?

If you’re looking for someone who can untangle the knots of business law, safeguard your personal matters, or help you sail through maritime complexities (with a touch of humor along the way), Siddhant’s your guy.

📩 Reach him at siddhantjain2403@gmail.com